Language

Service Enables Value Creation

Release Date:2013-03-15

By Li Zheng

In 2012, telecom operators didn’t benefit from thriving OTT businesses. As mature markets have become saturated with communications services and technologies, growth in core telecommunications businesses has stagnated and demand for network capacity has skyrocketed. Operators have been forced to invest in upgrading their infrastructure in order to satisfy this demand but have not reaped any of the financial reward from the services that their infrastructure hosts. Declining revenue and increased costs have weighed on the profit margins of operators. How, then, should an operator react, and should professional service providers adjust their strategies?

Strategic Transformation in the New Economic Environment

In October 2012, OVUM published its annual Telecoms Trends for 2013. The report indicated that in the sluggish global economic environment, operators will invest modestly but will come under greater pressure in terms of opex. To optimize costs, operators should strengthen network QoS and customer experience management. Suppliers should also change their roles from traditional equipment suppliers to network management service providers. To counter challenges from OTT businesses, operators should develop new business models and unearth new revenue sources by analyzing customer data.

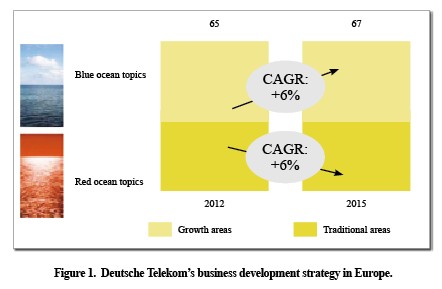

In December 2012, Deutsche Telekom revealed its corporate strategy for the next three years. DT’s operations will be divided into sustainable blue ocean business and shrinking red ocean business. The company plans to increase capex and opex for blue ocean businesses, and it plans to cut down opex for red ocean businesses by improving efficiency. Over the next two years, DT estimates a compound annual growth rate of 6% for its blue ocean businesses and -6% for its red ocean businesses.

DT has incorporated mobile broadband, connected home, and corporate ICT services into its blue ocean business. Traditional voice and SMS have been incorporated into its shrinking red ocean business.

Value Creation Is the Core of Professional Services

Increasingly, operators have been offering professional services in conjunction with their basic network infrastructure to create value for upstream and downstream customers.

To improve customer experience management (CEM), operators need to deploy related CEM platforms and data probes. Management methods, work flows, and employee skills also need to be upgraded in the transformation from network-oriented to customer-oriented operation. Equipment suppliers cannot merely provide software and hardware systems; they should provide professional services to help operators perfectly combine systems and processes for effective CEM.

Professional services are an important catalyst for the development of blue ocean business.

● CEM Professional Services

In the mobile internet era, customer experience has become a new driver of business growth, and traditional approaches based on optimizing network KPIs are no longer adequate. The focus has shifted to the customer and continuously improving customer experience. This strategy is fundamental for blue ocean business and allows operators to retain old customers, attract new customers, and increase revenue.

When building an end-to-end customer experience assurance system, operators should consider system, process, management, and personnel. First, the right tools should be used within an OSS/BSS environment to acquire, manage, and improve customer experience KPIs. Second, standard processes, such as ITIL and eTOM business processes, are required to re-orientate an operator from network KPIs to customer experience. Third, CEM involves every department: Only through concerted effort can customer experience be guaranteed. Last, the biggest hurdle in an operator’s transformation may be organizational culture. Key employees within the company need to be focused on the customer; only then can the company as a whole move in this direction.

Service providers should consider these four aspects and refer to their best practice experience when providing end-to-end customer experience assurance solutions to operators. An isolated solution cannot help operators maximize benefits.

CEM professional services for mobile networks should include consulting on the value of network traffic, managing the improvement of customer experience, managing the improvement of mobile quality, and managing the improvement of network performance. For fixed broadband, a multilevel, integrated service solution should be provided. Such a solution includes managing fixed terminals/family network, improving overall performance of fixed broadband network, providing OAM based on traffic value, and improving QoS. These help operators create a smart, highly efficient broadband network.

● DC Professional Services

The data center (DC) is the foundation of an entire modern IT system and is the key to an operator’s core competitiveness. Marketing and branding tend to be overtly tied in with the company’s core values, in a way that engineering and maintaining DCs is not. An operator needs assistance to develop IT strategies that align with the company’s core values. According to the OVUM 2012 Global Telco Data Center analysis, as operators expand their businesses globally, time-to-market (TTM) demands become more urgent, and there is an increased need for partners who can provide DC services.

DC service providers should provide quick TTM, reduce overall energy consumption, downsize IT facilities, consolidate the data center, and provide flexible network capacity. All these things help reduce costs. Service providers should develop core competencies in power usage effectiveness (PUE), DC design, modularization, safety management, and visualized management.

Reducing Costs Requires New Approaches

As networks expand rapidly and traditional business revenue shrinks, operators need to explore new approaches to optimizing opex and increasing profit margins.

● Managed Services

Traditionally, the scope of telecom business has been network engineering, OAM, marketing and branding, and charging. These areas comprise most of the entire vertical value chain.

Five to seven years ago, reducing opex and boosting management efficiency meant outsourcing the end part of the value chain, which includes OAM and construction of network infrastructure. With global network operations centers and by virtue of their size, a service provider could cut OAM costs and quickly acquire technical experts. Service providers and operators achieved good results together in this first period of service outsourcing.

Now, new technologies, such as LTE, IMS, CDN and PTN, are being used and may even co-exist in the network. This makes network OAM, troubleshooting, and timely provision of services more difficult.

In light of the successful first period of outsourcing, operators are seeking to outsource all network resource and business related activities. Supplier and contract management can be outsourced to a service provider, and the operator is the end-user’s single point of contact with the service provider. This helps operators simplify internal management and makes their operations leaner.

● Energy Management Services

According to statistics from Detecon, operators worldwide consumed about US$21.6 billion work of energy in 2012, about 10% of total worldwide network opex. To strengthen competitiveness, operators seek to reduce costs by better managing their energy consumption. Energy management accounts for a big chunk of opex, but it’s not the operator’s core business. Therefore, partners should think about how to provide better professional energy management services that align with market demands.

Energy planning, monitoring and optimization, including the management of KPIs, SLAs, equipment, and fuel chain, must be fully integrated. In the early stages of network construction, service providers should be focused on energy consumption over the network’s full lifecycle.

ZTE’s Service Business Is Growing Rapidly

Despite shrinking investment in the global telecom industry in 2012, ZTE’s service business grew 28% year-on-year. Over the past five years, ZTE’s service business has achieved a compound annual growth rate of 40%. ZTE’s managed service business maintained an impressive compound growth rate of 58% over this period.

Over the next two or three years, operators are very likely to continue reducing investment in network equipment because of the sluggish world economy. However, driven by the demands for updated technology, internal management, and business expansion, operators will increase their investment in service outsourcing. ZTE is a reliable partner that can help operators give their customers real value by providing customized solutions, global distribution channels, and fast delivery.

With global resources and solid marketing strategies, ZTE is optimistic about its service business and expects that the professional service business will grow more than 40% in 2013.

relative articles